The tsunami of turmoil created by the Global Financial Crisis may have felt unprecedented to many of us, but the fundamental lessons that emerged are now clear to all. The key takeaways for PE firms and the industry as a whole can be summarized as:

In 2008 the question was how to conduct deals, but in 2020 and beyond the question is where and with whom. We've all been through this before, or so we currently think.

PE Firms overexposed to industries crippled by COVID-19 like commercial real estate, travel, & hospitality are the only clear risks at present. But if 2008 taught us anything, it's that the best deals moving forward will have to be in the worst industries. Given the current monetary climate across the world, business models that are still operational, or more commonly flourishing, shouldn't have any issue capitalizing, which lays the groundwork for the tensions that will define investments in coming years.

In our analysis three distinct dangers then emerge. These are the lessons we can't learn, or haven't yet learned:

These are the known unknowns which we believe will define industry winners and losers in the coming years.

Usually a financial crisis brings the Great Depression or the 2008 meltdown to mind. But what is more germaine to our present moment is the M&A overleveraging of the 1980s. According to experts, "One part of the story (in 2008) is private equity-owned businesses weren't leveraged like they were in the 1980s at 90-10 (debt to equity) or even 95-5; it was more like 70-30." Presently the market was certainly more frothy than it was going into 08.

More loans across industry verticals are expected to default in coming months. The default rate of U.S. leveraged loans increased to 3.7 percent at the end of June, up from 2.0 percent in March, according to Capstone. That's the highest it's been since September 2010. For historical perspective, 8.5percent was the norm during the Great Recession. As the pandemic persists and stimulus efforts abate, fund managers expect default rates to tick higher and reach 5.3 percent by the end of the year, according to Capstone predictions. Three-quarters of economists surveyed by the National Association of Business Economics forecast a recession in 2020-21.

None of this is news to most market observers, but COVID-19 has thrown an entirely new dimension into the debt cycle and occasionally inflamed the geopolitical crisis we're all used to. "They have been waiting for this type of market dislocation," the head of mergers at a major Wall Street firm told CNBC in March 2020, "I don't think they wanted something quite this bad, but they did want a pullback in valuation."

Market dislocation means many businesses are struggling, and that's a great opportunity for VC and PE firms to invest in them. "Vulture investors, especially in private equity, are waiting in the wings to scoop up scores of struggling businesses on the cheap," says Rohit Chopra, an FTC commissioner. While not necessarily a glowing review of the industry from Chopra, it is true that outsized portfolio returns are often born from good deals.

In the COVID-19 landscape before us, it makes sense to look back to try and determine which strategies are best moving forward for PE.

Because private equity usually has a pre-existing relationship with many different types of businesses and access to capital, the industry will have a huge advantage in the years and months to come. "There is plenty of capital on the sidelines, and it's really the private credit asset managers who are driving this market and financing the acquisitions," says Ted Koenig, president and CEO of Monroe Capital.

The rules of investment seem to hold true no matter where you find yourself globally. In reviewing the crisis, it was found that UK-based private equity-owned businesses outperformed their peers during the crisis in relation to most metrics: investments made, cost of debt, asset growth and operational support from the financial backer.

It's likely now a good time to start thinking strategically, as leveraged lending levels fell by 80 percent from January through April 2020, according to Dealogic.

"The global financial crisis was the first real test of the private equity model. Could they refinance their existing portfolios, not to mention do new deals?" said Peter Witte, EY's global lead private equity analyst, in an interview with Institutional Investor. "There were concerns at the time. But we saw that PE-backed companies ultimately suffered fewer defaults and invested more (in their businesses) than companies not backed by PE."

Buying low and selling high works- there's a reason it's the lynchpin of any PE strategy.

Operational assistance to portfolio companies generates the best IRR in the previous downturn. Management, marketing, and other technical assistance that a firm can provide to a portfolio company only ends up with a positive net; the data confirms this.

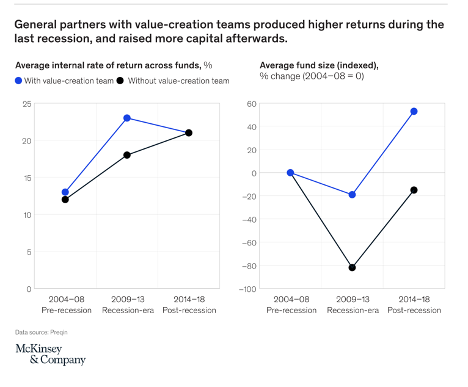

During the recession, McKinsey found that firms with value-creation teams "meaningfully outpaced the others, achieving a full five percentage points more in IRR (23 percent) than firms without portfolio-operating groups (18 percent)."¬ù Before and after the crisis, both groups of firms performed comparably (about 13 percent net internal rate of return (IRR) for vintages 2004-08 and about 21 percent for vintages 2014-18).

According to experts, there's a 5+ year horizon for patience, time that can be spent supporting businesses through an economic downturn, leaving them ready for a sale on the other side of things. Conversely, bank lending seems to be another story. Many observers believe banks are too distracted with administering the Paycheck Protection Program and the Main Street Lending Program to compete effectively.

Thinking about add-on acquisitions in the context of operational excellence is essential. Add-on acquisitions made up the highest percentage of buyouts on record, according to Pitchbook Data. In 2008, generally only the larger firms had operating expertise. Now, most portfolio companies can get help for their acquisitions with supply chain issues and other day-to-day challenges. General partners that focused on portfolio company operations had more success fundraising between 2009 and 2013. McKinsey reported that average fund size declined 19 percent for these firms, versus an average decline of 82 percent for private equity firms without value-creation teams. Currently, PE firms have 30% more operating partners than they had just five years ago. Let that sink in, and plan your strategy accordingly.

Opportunities were lost in 2008 from a lack of action. "Leadership teams were not prepared to navigate a systemic collapse. No-one was. To lead through future crises, leaders must hone their team's ability to be responsive and nimble; they need to mobilize their people with speed and agility," says Russel Reath, President of Kotter Consulting.

Diversification and trying out new fields of competition are a must, with the express intent of staying agile. "This trend towards PE groups moving into areas such as CLOs, is something we've been seeing for a couple of years," says Trevor Headley at FIS Global. "Firms see this as a mid-term opportunity to generate returns over and above what they are seeing across other asset classes."

We can only expect that financial mechanisms will become more sophisticated as PE firms get more creative about how to spread risk and increase returns. There are a great deal of experienced and weathered managers at the tiller of many PE firms, so the market will be more difficult to navigate. Geopolitical unrest will definitely be a factor as well. "As a result of that, private equity has really focused on value generation as well as value preservation. And that is, I think, one of the big differences with the situation today compared to 2008," says Thiha Tun, Dechert private investment funds and transactions partner.

Private equity's secondary market has also matured and evolved to a point where general partner-led restructurings, once seen as an embarrassing sign for both GPs as well as LPs delivering the news to their investment committees, are now seen as attractive options to extend fund life and offer liquidity to investors. Keep an open mind, stay agile, and don't forget Lesson #1.

PE firms in the US have more than $1.4t in immediately deployable funds, and when other adjacent asset classes are added - credit, infrastructure, real estate, growth capital etc. - the aggregate amount of committed capital PE can readily deploy stands at more than US$2.6t.

And what then? Well, the big question that many PE firms have to consider is are they behaving too conservatively. Knowing that capital is best used for investment is an ever-persistent lesson and danger in finance. Like the stock investor that is wondering why they didn't buy tech stocks in late March, that war chest may have missed its moment. Right now it's unclear. 2021 may bring great deals in great industries, but it also may not.

There is always the danger of over-specialization. In times of economic downturn, sector generalists do better because downturns hit sectors asymmetrically. But it is also possible to be too conservative, like Danger #1. The most important thing to be aware of is what you're getting yourself into. Specialized investments and firms geared towards them can see huge potential upsides in centralized expertise. Even if you're not exposed to industries fundamentally ruptured by COVID-19, this crisis has emphasized the central pitfall of specialization.

During the period ending in June 2019, the drop in one-year IRRs was driven by venture capital and secondary funds. According to Pitchbook's recent global fund report, venture capital IRRs had been in decline for more than a year, dropping from the 20 percent range in 2018 to 13.9 percent for the year ending in June 2019. Despite this sharp decline, venture capital funds were the highest-performing private capital funds for the fifth-consecutive quarter, according to PitchBook.

By comparison, the S&P 500 delivered 14.7 percent annualized over the same period. According to PitchBook, private equity's "high correlation with and underperformance of public markets during the last decade has caused some LPs to cry foul and question PE's place in institutional portfolios."

The economic downturn signifies the death knell for industries already reeling from the disruption in the last decade. As far back as 2019, industry leaders were already lamenting that many people are returning to the bad behavior of 2007-08, but worse.

Pricing levels have stabilized, if not declined a bit, since the April/May timeframe, as the expected rush of high-rate opportunistic deals did not materialize. Funds started in 2006, around the pre-recession market peak, returned a median 8.1 percent, while those with a 2009 vintage delivered 13.9 percent. The question for PE firms right now is which side of that dip did we start on, and are we still yet to stare down a deeper dip?

Be wary of the sectors with little to no activity: hotels, auto, airlines, entertainment and some consumer sectors, telecommunications and oil & gas. Some of these sectors are already experiencing issues with their loans. Telecommunication comprises about 20 percent of leveraged loan defaults, followed by oil & gas (about 13 percent) and retail (about 12 percent), according to Capstone Headwaters. (As we mentioned earlier, the average default rate across industries was 8.5% during the Great Depression)

"For strong sectors little has changed. Private credit vehicles raised $57 billion in the first half of the year, according to Preqin. Privately-owned companies continue to raise capital in the debt market, despite the disruption caused by Covid-19, the recession, and the falloff in the energy market," says Kent Brown, a managing director and head of Capstone Headwaters' Debt Advisory Group. "Every day that goes by, the market seems to be normalizing. It has not recovered for sure, but the trends are going in the right direction. We don't think the market will get back to where it was in January anytime soon."

As a rule of thumb, the businesses that have been attracting money from lenders are those that have proven they are largely Covid-19-protected. If nothing changes in the current market, that means that the deals which materialize in 2021 may be extremely risky and stable deals may have an even higher valuation.

Prior to Covid-19, the private equity industry was seeing serious gains. In fact, global private equity deal value in 2019 reached $551 billion, according to Dealogic.

Contrast that to what is happening now. The number of funds that have closed so far in 2020 is down 50% year-on-year while the dollar value of capital raised remains steady, according to PEI data.

"Corporate debt as a percentage of gross domestic product is now at the highest peak we've ever had," says Edward Altman, Professor Emeritus of finance at NYU's Stern School of Business. The value of corporate debt hit 47% of gross domestic product this year, higher even than the 45% it hit in 2008 before the last recession. More than half of investment-grade debt was rated BBB last year, at the edge of junk territory, and about 30% of that was vulnerable to a downgrade before the coronavirus outbreak.

That means high default rates. The number of zombie companies likely to fail within 12 months has likely doubled. The commercial mortgage-backed securities market has essentially collapsed and the broader $20 trillion commercial real estate market is on the verge of collapse as well, according to Greg Kraut, co-founder and CEO of New York-based KPG Funds. "We still have time to prevent this catastrophic event, but we need government intervention now," Kraut wrote on April 2 in a column for the Commercial Observer. The broader market conditions surrounding current portfolio companies are far from ideal.

There are many ways getting bad press can reduce the chance of a bailout and the chance of attracting investors. Toys 'R' Us is the poster child for these losses, with Lerner and Colleagues recording a 6 percent rate of job loss at private equity-backed retail companies from 1980-2000. While these numbers have been disputed PE did not have a great public reputation before this latest crisis and firms certainly need to continue the potential dangers of populist political agendas on either side of the aisle.

It doesn't look good to be footing the bill for poorly run companies, so the name of the game is always stay nimble, and stay smart.

2008 wasn't the first financial crisis in history. Ultimately it may not have shaken some industries as thoroughly as the tech bubble of the early 2000s, or been as long lived as downturns in other decades. But the GGC was unprecedented for the speed with which a technologically anchored economy indecipherably ruptured across the globe. LPs are certainly weighing the lessons from those years carefully at present. While the operational template seems clear, buy low & sell high, drive operational excellence, and move quickly, the unknowns at present are where and when to direct those efforts.

To paraphrase Tolstoy, bull markets are all alike; every economic downturn is opaque in it's own way. Plagues are not a new crisis for humanity. But at present 2021 will certainly indicate whether firms were able to leverage their vast assets at the right times, mitigate risk, and move beyond the shaky ground that was already taxing them before this crisis.

If you're interested in finding better investment opportunities and sourcing better deals, no matter what the economic climate, our deal origination platform may be of interest. Request a demo to find out how upgrading your research process with our innovative M&A platform can help you find what good deals there may be.