Who remembers calling the local movie theater to check showtimes? What about getting up off the couch every time you wanted to change the television channel? Or how about dropping a roll of camera film off to be developed sometime in the next week?

Now we have movie theater mobile apps that conveniently list play times, remote controls that switch channels from across the room, and digital cameras and printers that produce beautiful photos in seconds. Processes and technologies have evolved to enable humans to accomplish far more in a fraction of the time "and investment banking deal origination is no exception.

Let's take a look at traditional deal origination, and then discuss some of the top dos and don'ts modern firms are following to enhance efficiencies and improve investment banking deal flow.

Deal origination is the process by which banks identify promising investment opportunities. Traditionally, most deals have come inbound from a colleague or acquaintance, and dealmakers have had to research the company and vet whether or not it's a good opportunity. Today, more deals originate based on outbound efforts, when firms actively search for opportunities that match specific investment criteria and domain expertise.

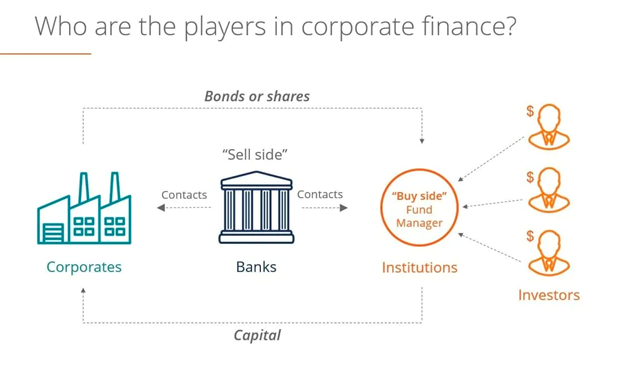

It's important to remember that investment banks function as intermediaries and help manage deals on both the buy-side and the sell-side. The buy-side refers to working with private equity firms to find companies for them to invest in or buy. The sell-side involves working with companies looking to raise funding or sell.

This two-sided equation makes deal origination an even more complicated process for investment banks. Fortunately, advancements in data and technology have given way to a new set of rules that new school firms are following to find and close more of the right deals faster.

A bank's deal origination strategy once depended on having members with established reputations and expansive Rolodexes. Golf games and lunch meetings were firms' top deal sources. But over time, it became clear that networking alone is not a consistent or repeatable way to generate investment banking deal flow.

In today's fast-paced and highly competitive market, firms need a more predictable and proactive approach. Rather than waiting for introductions to companies that may or may not be good fits, direct sourcing allows banks to take control of their deal flow by actively seeking out specific, high-potential opportunities. But it wasn't until recently that technology transformed direct sourcing from a painstaking manual exercise to a highly efficient and data-driven process.

Using the latest M&A technology, investment banks can quickly filter through millions of companies and associated data signals to pinpoint investment-ready companies that align with their clients' investment theses. This includes companies from the pre-transacted universe, which are harder to find and more likely to provide firms with proprietary investment opportunities. Here are just a few sample data points firms can access:

"Data" and "relationships" may not seem like they belong in the same sentence, but with access to signals like those listed above, modern firms are using data to foster the right relationships much faster. In fact, with so much data available, people are actually becoming frustrated when experiences and communications aren't personalized!

First, it's important to ensure that the companies you're taking time to engage with are the best possible fits for your private equity clients. Automated lead scoring makes it easy to identify the businesses that are the most relevant by assigning weights to various data points firms may consider, and then ranking potential opportunities accordingly.

Once a bank has identified its top targets, it can dig deeper into the data to personalize all communication with these opportunities, from congratulating them on a new executive hire to acknowledging their local baseball team's big win. The same tactic can be used to customize outreach to private equity firms around sell-side opportunities by digging into the types of companies in their current portfolios.

This data-driven approach can also be combined with investment banking conference strategy. Rather than simply attending every big-name trade show on the calendar, use a private company intelligence platform to figure out which conferences are hosting your top targets and get smart on these companies. Sending personalized notes increases your chances of booking a conference meeting or lunch, and also prepares you to stand out from the competition during expo hall conversations.

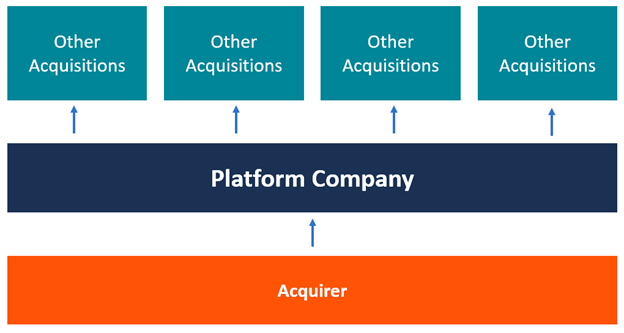

Add-ons are investments firms make in smaller companies to add value to larger platform investments. As faster, less-expensive, and lower-risk investments, add-ons are growing in popularity, with 40% of private equity firms planning to incorporate them into their core strategies.

Although add-ons amplify platform investments, more banks are beginning to identify add-ons earlier in the investment banking process during the platform company research phase. This is made possible by new solutions that aid in the traditionally time-consuming and error-prone market mapping process. These tools surface detailed, verified company information that allows dealmakers to rapidly generate more comprehensive and accurate market maps.

Recommending potential add-on investment opportunities when pitching platform companies to PE clients empowers firms to better illustrate the long-term value of particular investments and negotiate better deals. Highlighting these opportunities early in the buy-side dealmaking process also sets the stage for potential follow-on deals and recurring business. Similarly, using data services to pinpoint which firms have recently invested in platform companies in a given segment enables banks to rapidly pitch sell-side clients as potential roll-ups or bolt-ons.

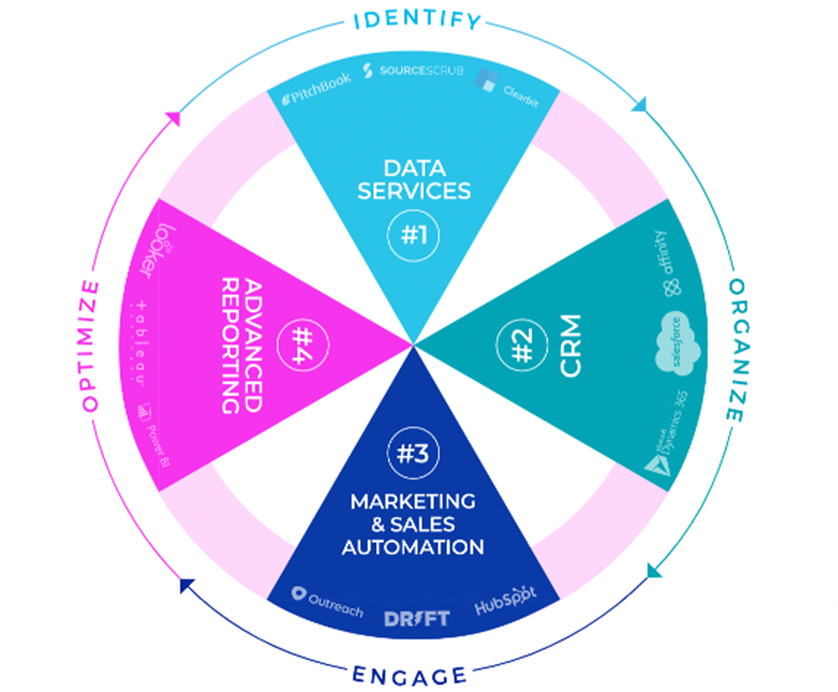

Private company intelligence platforms are just one of the technologies teams can use to accelerate investment banking deal origination. Modern firms are building advanced, fully-integrated ecosystems of solutions (AKA "tech stacks") to help automate administrative tasks, rapidly scale workflows, turn data into proprietary advantages, and much more.

Every tech stack is different, but there are four core components we recommend most investment banks invest in adopting and integrating:

To learn more about each of these four components, how they work together, and the best ways to build your stack, try downloading this free guide.

Risk and reward are two sides of the same coin. Institutions are more effective at anticipating change and achieving the right outcomes if they don't consider strategy and risk management as separate and parallel. The recent global pandemic and supply chain issues have proven this to be truer than ever.

Investment banking risk management begins and ends with the software, technology, and market analysis tools banks bring to the table. For example, market analysis informs everything from your deal sourcing efforts to finding strategic buyers in M&A. By having as much information as possible on potential leads and firmographic data at hand, you can lessen the amount of risk you take on due to lack of insight.

Asymmetric information typically occurs when the buy-side is less informed than the sell-side, resulting in an improperly proposed deal. Fortunately, the latest private company intelligence tools offer target market analysis functionality that helps investment banks reduce and manage risk by providing key insights about different financial markets.

You wouldn't buy a TV with no remote control, or use a low-speed dial-up internet connection. You leverage modern technology to live a more convenient and productive lifestyle.

Similarly, investment banks must also take advantage of the latest data, tools, and processes to source more of the right deals faster. Those that don't are at risk of being outpaced and outperformed by more modern competition.

To learn more about these dos and don'ts and how to source deals using the latest and greatest technology, download the free guide, Think and Grow Different: Dealmaking Strategies for Investment Banks.