Understanding a company's value entails navigating through diverse methodologies, especially when it comes to evaluating private enterprises. With numerous valuation models available, it's essential to grasp their nuances and applications, particularly in the context of private company assessments.

In this article, we share insights gleaned from assisting M&A professionals in adopting data-driven strategies for analyzing bootstrapped company revenue growth and investment readiness. Join us as we delve into the most popular valuation models tailored specifically for private companies.

Valuation models are used to determine the worth or fair value of a company. Analysts take dozens of factors into consideration depending on the valuation method used including income statements, balance sheets, market conditions, business models, and management teams. Getting the most accurate estimate requires the use of several different types of valuation methods and analyses, each of which has its own strengths, weaknesses, and appropriate use cases.

However, it's important to keep in mind that company valuations aren't entirely scientific. As James Faulkner, managing director at London-based VC firm Vala Capital says, "There is still a huge amount of art involved because the financial model [for valuing the company] will depend entirely on subjective inputs: estimates for everything from the rate of sales growth to the company's salary costs for the next five years."

Getting as close as possible to an accurate estimate of company value is critical to both business owners and investors.

Business owners care about valuation when they want to:

Investors, such as private equity (PE) firms or investment banks, care about valuation when:

It's much easier to determine the value of a public company than a private company. Unlike private businesses, public companies must adhere to strict accounting protocols and report on their financials on a regular basis. Determining the current market value of a public company is as simple as multiplying its share price by the number of outstanding shares, both of which are publicly listed on the stock exchange.

Many analysts also calculate the intrinsic value of public companies. This involves going beyond market value to include other intangible factors that may impact a company's true current and future worth, like patents and brand recognition. It uses fundamental analysis to look at both qualitative and quantitative factors. Intrinsic valuation is also called absolute valuation.

In contrast to absolute valuation, which looks at various factors related to a specific business, relative valuation attempts to determine the worth of a business based on where it stands compared to other companies in the same industry. While public companies may be evaluated using both absolute and relative methods, private companies may only be evaluated using the latter, since there is little to no financial data publicly available to establish intrinsic value.

There are a number of different relative valuation vs. absolute valuation techniques.

Absolute valuations leverage what's called discounted cash flow (DCF) analysis. The goal of DCF is to estimate the future cash flow of a given business to understand whether an investment will generate a positive return.

There are many subtypes of the DCF model, including:

The below video offers a breakdown of the DCF formula and how it might be applied in a real-life investment scenario:

Comparable company analysis (CCA) is the most common method used to value private companies. The first step is to establish a "peer group" of public companies in the same industry that share similar characteristics (e.g. employee count, age, etc.). Next, select a multiple, such as EBITDA, and calculate the average across these companies. This average is then assigned to the private company.

The estimated discounted cash flow method uses the same formula as the DCF absolute valuation technique above. However, it relies on average measurements from the private company's peer group to assess its weighted average cost of capital (WACC).

The precedent transactions method involves looking at how much companies in the same industry were sold or acquired for, and applies their average valuation multiples to the private company in question. It's important that these companies are as similar as possible to the given private company, and the analyzed transactions are recent. This is sometimes referred to as the "market multiple" method.

This method values a company based on what it would cost to build it all over again from scratch. While fairly straightforward to calculate, the cost to duplicate approach fails to consider intangible assets and future revenue potential, which are both key for private growing companies.

This is a rough estimate technique often used by early-stage angel investors. It essentially assigns value ranges based on various company milestones, such as developing a market-ready product or cultivating a customer base.

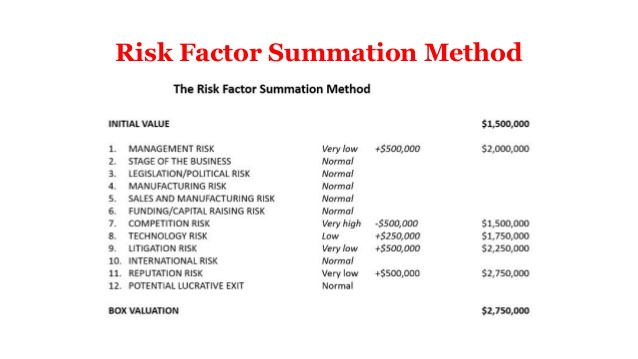

The risk factor summation method is a risk-based valuation technique that assigns points and associated dollar values to 12 specific categories, including litigation risk, competitive risk, and reputation risk.

Because numbers around revenue and growth aren't publicly available for non-transacted companies, investors must use other data points to identify peer groups and leverage relative valuation techniques. However, even this exercise can be a challenge. Dealmakers often spend countless hours scouring the internet for accurate bootstrapped company information.

Fortunately, the latest data service providers are making private company data readily available to investment teams. Sourcescrub recommends dealmakers pay attention to these 9 core data signals:

In addition to identifying relevant peer groups and informing traditional valuation methods, easy access to data points like these empowers firms to develop proprietary models and projections around founder-owned company size, growth, and value.

There are various company valuation methods available, each blending elements of both art and science. While accurate valuations are crucial for both business owners and investors, assessing the value of a public company is typically more straightforward and transparent compared to private counterparts.

Private company valuations heavily rely on relative valuation techniques, where a private entity is compared to similar public companies within its industry. However, acquiring the necessary data to construct these peer groups, conduct traditional valuations, and generate proprietary projections can be challenging.

In response, modern dealmakers are embracing the latest data and technology to gain deeper insights into founder-owned businesses swiftly. This approach not only aids in thesis development and company valuation but also offers numerous other benefits. For further exploration of this topic, delve into our New School Manifesto.

Originally posted on "November 9th, 2021"